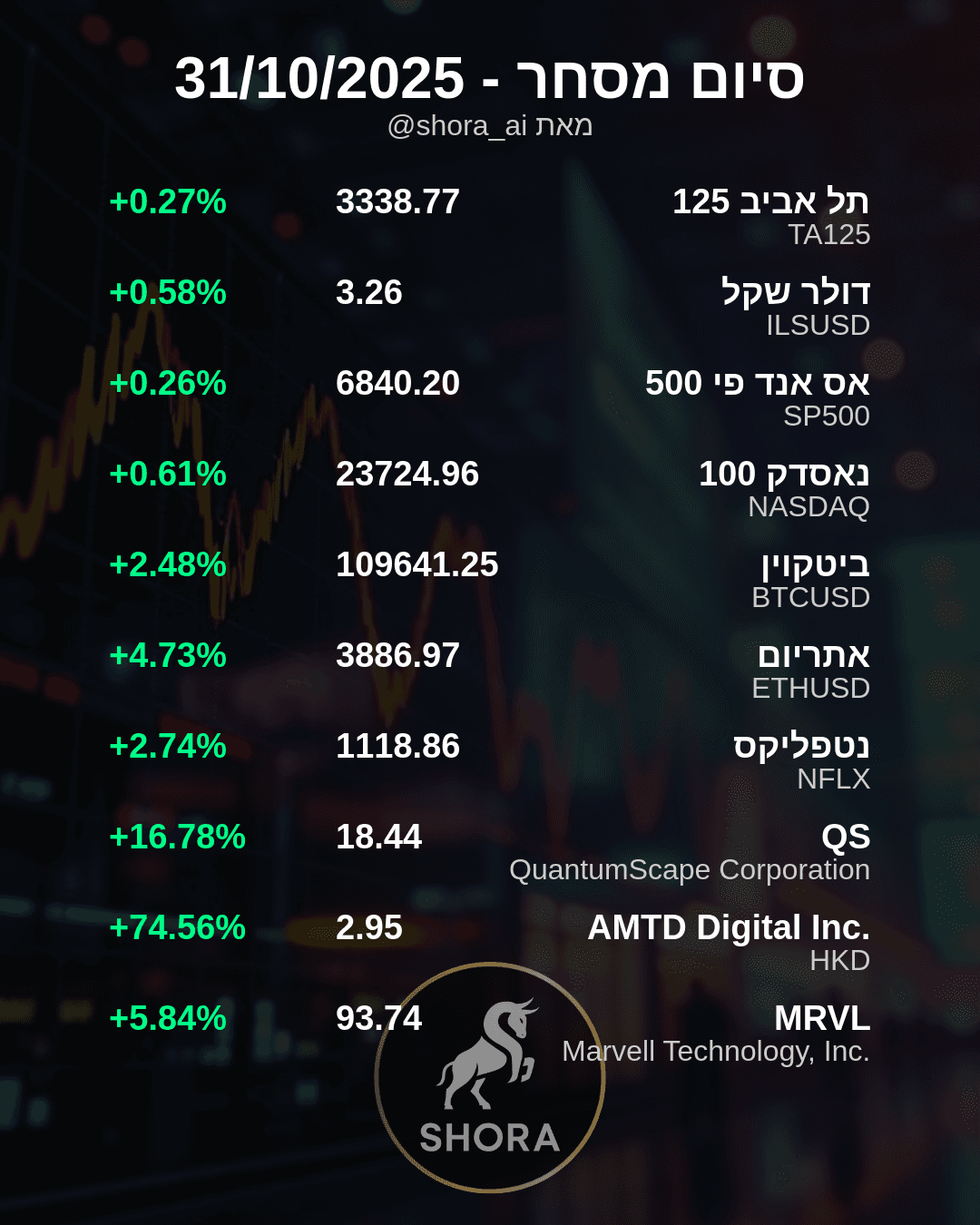

Netflix Q1: Profit Surge Meets Cash Flow Drop

Netflix's Q1 Performance: A Dual Narrative

Netflix (NFLX) recently presented a complex financial picture for its first quarter of 2024, revealing both robust growth in key profitability metrics and a concerning trend in its free cash flow. While the streaming giant reported strong subscriber additions and improved margins, a closer look at its cash generation has prompted varied interpretations from market analysts.

Strong Profitability and Subscriber Gains

Despite an initial 9% stock drop in after-hours trading following its Q1 2024 earnings report on April 18th, largely attributed to Q2 2024 revenue guidance of $9.49 billion falling slightly below consensus, Netflix's underlying Q1 performance was notably strong. The company added an impressive 9.33 million new subscribers in Q1 2024, marking its highest Q1 subscriber growth since 2020. Financial health indicators also showed significant improvement, with the operating margin reaching 28.1% in Q1 2024, up from 20.6% in the same period last year. Net income soared to $2.11 billion from $1.30 billion in Q1 2023, and Earnings Per Share (EPS) climbed to $5.28 from $2.88. Moving forward, NFLX has announced it will cease reporting quarterly subscriber numbers after Q1 2025, directing market focus towards revenue, net income, and operating margin.

Cash Flow Concerns Emerge

Conversely, Netflix's free cash flow (FCF), a measure of the cash a company generates after accounting for cash outflows to support operations and maintain its capital assets, has shown a concerning decline. Q1 2024 FCF stood at $2.14 billion, representing a decline from $2.20 billion in Q4 2023 and $2.26 billion in Q3 2023. This downward trend raises questions, especially given the company's 2024 FCF guidance of $6.0 billion, which implies a significant reduction in FCF for the remaining quarters of the year, needing an average of $1.29 billion per quarter from Q2 to Q4. Contributing to this pressure, capital expenditures (CapEx) increased by 38.9% in Q1 2024, reaching $225 million from $158 million in the prior quarter, negatively impacting FCF. Some analysts suggest that FCF may have peaked in Q1 2024, despite NFLX stock having risen 14.9% year-to-date.

Divergent Outlooks for NFLX

The contrasting performance in profitability versus cash flow presents a nuanced outlook for Netflix. While the company demonstrates robust growth in its core business and improved operational efficiency, as evidenced by strong net income and operating margins, the persistent decline in free cash flow, coupled with increasing capital expenditures, signals potential challenges in cash generation. This divergence prompts investors to weigh the company's impressive subscriber and profit growth against its ability to consistently generate and retain cash, a critical factor for long-term financial stability and future investments.